Downloading and Analyzing Stock Data with fintorch

![]()

In this tutorial, we’ll explore how to use the fintorch Python package to download historical stock data and prepare it for machine learning tasks. Specifically, we’ll focus on Apple (AAPL), Microsoft (MSFT), and Google (GOOG) stocks from January 1, 2015, to June 30, 2023. We’ll also discuss how fintorch integrates with the neuralforecast library by providing a TimeSeriesDataset that’s compatible with its data structures, making it easier to organize data for training,

validation, and testing.

Overview

The fintorch library is designed for financial data analysis and machine learning applications. It simplifies the process of downloading, storing, and preparing financial datasets. Under the hood, it uses yfinance to retrieve data from Yahoo Finance, ensuring a reliable and comprehensive data source.

One of the key features of fintorch is that it provides data in a TimeSeriesDataset format compatible with the neuralforecast library. This compatibility streamlines the process of organizing time series data for machine learning models, including handling train/validation/test splits.

Step-by-Step Explanation

Let’s break down the code to understand how each part contributes to downloading and analyzing the stock data.

[1]:

import logging

from datetime import date

from pathlib import Path

from fintorch.datasets import stockticker

Importing Modules:

logging: For logging information during execution.datefromdatetime: To specify the start and end dates for the data.Pathfrompathlib: To handle file system paths.stocktickerfromfintorch.datasets: Contains theStockTickerclass for handling stock data.

[2]:

# Set logging level to INFO

logging.basicConfig(level=logging.INFO)

Setting Logging Level: Configures the logging system to display messages of level

INFOand higher.

[3]:

# Parameters

tickers = ["AAPL", "MSFT", "GOOG"]

data_path = Path("~/.fintorch_data/stocktickers/").expanduser()

start_date = date(2015, 1, 1)

end_date = date(2023, 6, 30)

Defining Parameters:

tickers: A list of stock ticker symbols we’re interested in.data_path: The directory path where the stock data will be stored locally.start_dateandend_date: Define the time range for the historical data.

[4]:

# Create a dictionary mapping from tickers to index

ticker_index = {ticker: index for index, ticker in enumerate(tickers)}

Mapping Tickers to Indices:

Creates a dictionary that maps each ticker symbol to a unique index. This can be useful for referencing and organizing data.

[5]:

# Load the stock dataset

stockdata = stockticker.StockTicker(

data_path,

tickers=tickers,

start_date=start_date,

end_date=end_date,

mapping=ticker_index,

force_reload=True,

)

INFO:root:StockTicker dataset initialization

INFO:root:force reloading stock data from yahoo finance

[*********************100%%**********************] 3 of 3 completed

INFO:root:All datsets loaded sucessfully

INFO:root:loaded dataset:TimeSeriesDataset(n_data=8,655, n_groups=3)

Loading the Stock Data:

Instantiates the

StockTickerclass with the specified parameters.Parameters Explained:

data_path: Where the data will be stored.tickers: The list of stock symbols.start_dateandend_date: The date range for the data.mapping: The ticker-to-index mapping.force_reload=True: Forces the data to be re-downloaded even if it already exists locally.

Under the Hood:

The

StockTickerclass usesyfinanceto fetch the stock data from Yahoo Finance.It organizes the data into a

TimeSeriesDatasetcompatible with theneuralforecastlibrary.

[6]:

print(stockdata.df_timeseries_dataset.to_pandas().describe())

ds y unique_id

count 8655 8655.000000 8655.000000

mean 2020-02-26 03:56:05.407000 118.096947 1.000000

min 2015-01-02 00:00:00 20.697262 0.000000

25% 2017-11-10 00:00:00 49.313992 0.000000

50% 2020-09-24 00:00:00 103.036682 1.000000

75% 2022-07-15 00:00:00 155.169968 2.000000

max 2023-06-29 00:00:00 344.776672 2.000000

std NaN 80.441103 0.816544

Integration with neuralforecast

TimeSeriesDataset Compatibility

The stockdata.df_timeseries_dataset provided by fintorch is designed to be compatible with the TimeSeriesDataset format used by the neuralforecast library. This compatibility is significant because it:

Simplifies Data Preparation: The data is already organized in a way that’s suitable for machine learning models, reducing the need for additional data wrangling.

Eases Train/Validation/Test Splits:

neuralforecasthas built-in methods for splitting datasets, and having data in the compatible format allows you to leverage these methods directly.Facilitates Model Training and Evaluation: Consistent data formatting ensures smoother integration with

neuralforecastmodels and evaluation metrics.

Example of Using TimeSeriesDataset with neuralforecast

Here’s how you might proceed to use the dataset with neuralforecast:

[7]:

print(stockdata.df_timeseries_dataset.to_pandas())

ds y unique_id

0 2022-01-03 179.076599 0

1 2022-01-04 176.803833 0

2 2022-01-05 172.100861 0

3 2022-01-06 169.227921 0

4 2022-01-07 169.395172 0

... ... ... ...

8650 2023-06-23 122.718620 2

8651 2023-06-26 118.798248 2

8652 2023-06-27 118.718452 2

8653 2023-06-28 120.783379 2

8654 2023-06-29 119.716003 2

[8655 rows x 3 columns]

[8]:

from neuralforecast import NeuralForecast

from neuralforecast.models import NBEATS

# Initialize the model

model = NBEATS(input_size=30, h=7)

# Create a NeuralForecast object

nf = NeuralForecast(models=[model], freq='D')

# Define validation and test sizes

val_size = 100 # Number of days for validation

test_size = 100 # Number of days for testing

# Perform cross-validation

Y_hat_df = nf.cross_validation(

df=stockdata.df_timeseries_dataset.to_pandas(),

val_size=val_size,

test_size=test_size,

n_windows=None # Uses expanding window if None

)

Seed set to 1

GPU available: True (cuda), used: True

TPU available: False, using: 0 TPU cores

HPU available: False, using: 0 HPUs

You are using a CUDA device ('NVIDIA GeForce RTX 3090') that has Tensor Cores. To properly utilize them, you should set `torch.set_float32_matmul_precision('medium' | 'high')` which will trade-off precision for performance. For more details, read https://pytorch.org/docs/stable/generated/torch.set_float32_matmul_precision.html#torch.set_float32_matmul_precision

LOCAL_RANK: 0 - CUDA_VISIBLE_DEVICES: [0]

| Name | Type | Params | Mode

-------------------------------------------------------

0 | loss | MAE | 0 | train

1 | padder_train | ConstantPad1d | 0 | train

2 | scaler | TemporalNorm | 0 | train

3 | blocks | ModuleList | 2.4 M | train

-------------------------------------------------------

2.4 M Trainable params

555 Non-trainable params

2.4 M Total params

9.786 Total estimated model params size (MB)

Epoch 999: 100%|██████████| 1/1 [00:00<00:00, 48.77it/s, v_num=12, train_loss_step=2.200, train_loss_epoch=2.200, valid_loss=2.410]

`Trainer.fit` stopped: `max_steps=1000` reached.

Epoch 999: 100%|██████████| 1/1 [00:00<00:00, 45.46it/s, v_num=12, train_loss_step=2.200, train_loss_epoch=2.200, valid_loss=2.410]

GPU available: True (cuda), used: True

TPU available: False, using: 0 TPU cores

HPU available: False, using: 0 HPUs

LOCAL_RANK: 0 - CUDA_VISIBLE_DEVICES: [0]

Predicting DataLoader 0: 100%|██████████| 1/1 [00:00<00:00, 269.38it/s]

/home/marcel/Documents/research/FinTorch/.conda/lib/python3.11/site-packages/neuralforecast/core.py:199: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

warnings.warn(

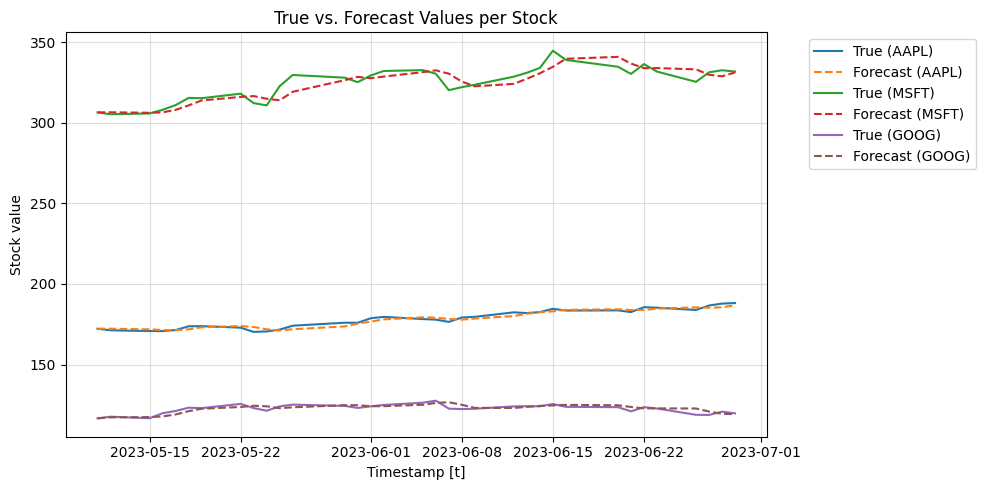

Here we plot the mean prediction of the cross validation function for the 4-folds

[10]:

import matplotlib.pyplot as plt

plt.figure(figsize=(10, 5))

# Iterate through each unique stock using the index

for unique_id in Y_hat_df.index.unique():

stock_data = Y_hat_df.loc[unique_id] # Index-based selection

stock_data = stock_data.reset_index().groupby('ds').mean().reset_index()

# Plot true values and forecast for the current stock

plt.plot(stock_data['ds'], stock_data['y'], label=f'True ({tickers[unique_id]})')

plt.plot(stock_data['ds'], stock_data['NBEATS'], label=f'Forecast ({tickers[unique_id]})', linestyle='--') # Dashed line for forecast

# General plot formatting

plt.xlabel('Timestamp [t]')

plt.ylabel('Stock value')

plt.title('True vs. Forecast Values per Stock')

plt.grid(alpha=0.4)

# Adjust legend to fit better

plt.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

plt.show()

Understanding yfinance

yfinance is a Python library that provides a convenient way to download historical market data from Yahoo Finance. It supports a wide range of data, including:

Historical prices

Dividends

Splits

Financial statements

In this tutorial, fintorch leverages yfinance to handle the data retrieval of stocktick data, making it seamless to obtain and work with financial datasets.

Conclusion

By following this tutorial, you’ve learned how to:

Set up logging for better debugging and information tracking.

Specify parameters for data retrieval, including tickers and date ranges.

Use

fintorchandyfinanceto download historical stock data.Obtain a

TimeSeriesDatasetcompatible withneuralforecast, simplifying the process of preparing data for machine learning models.

This foundational knowledge can be expanded upon for more complex analyses, such as building financial models or integrating advanced machine learning algorithms.

Next Steps

Explore the Data: Use visualization libraries like Matplotlib or Seaborn to plot the stock prices and observe trends.

Feature Engineering: Create additional features such as moving averages, volatility indicators, or technical analysis signals.

Model Training: Use the prepared

TimeSeriesDatasetto train machine learning models usingneuralforecastor other libraries like TensorFlow or PyTorch.Model Evaluation: Implement evaluation metrics to assess the performance of your models on validation and test sets.